Graphene is seen as the Wonder material of 21st Century due to its extraordinary properties as well as the wide applications in various downstream areas such as energy, electronics and bioengineering. However, extremely high cost and potential pollution during the production process are the major restraints of graphene’s large-scale commercialization, thus finding a cost effective and sustainable way to produce synthetic graphite and graphene has become more urgent. Frost & Sullivan has conducted extensive investigation across the global graphite and graphene industry chain, and released the White Paper for Global Graphite and Graphene Markets, which focus on the recent development of global graphite and graphene industry as well as the new growth opportunities.

Based on Frost & Sullivan’s investigation and calculation, the global market size of graphite was USD22.0 billion in 2021, of which the Asia-Pacific region, North America and Europe accounted for 44.1%, 27.3%, and 18.6%, respectively. The global graphene market size was USD12.6 billion in 2021, with Asia Pacific, North America, and Europe accounting for 54.4%, 21.2%, and 20.0% respectively. The global graphite and graphene market is expected to reach USD30.4 billion and USD71.9 billion, respectively in 2026.

Electronics and energy are the main sectors for graphene applications. Now graphene is commonly used as a heat-dissipation material in the electronics field and a conductive material in the energy field. The graphene market size in the electronics and energy industry is expected to grow at a CAGR of 35.2% and 32.6% from 2022 to 2026. In the future, the automotive industry is the most promising segment of graphene, which is expected to grow at a CAGR of 42.1% from 2022 to 2026, according to Frost & Sullivan.

Major economies globally including the EU, the U.S., and China have all issued a series of graphite and graphene related favorable policies, creating a good policy environment for graphite and graphene’s development. Favorable policies are the fundamental preconditions for the development of the industry with strategic importance or emerging industries such as graphite and graphene, which can attract abundant resources from both the financial side and the industrial side. Except for the policy support, the diversified downstream applications, especially the disruptive applications demonstrate the enormous commercialization potential of graphene and drive.

However, the White Paper also indicates that the graphite industry is facing the pain points of uneven distribution of natural graphite resources and high pollution in the production process, while the graphene industry has pain points such as high production costs, high energy consumption, and high pollution. Hence the commercialization process of graphene is relatively slow, and the high-end applications of graphene such as biology, semiconductors, and other fields are still waiting for substantial technology breakthroughs to increase production efficiency and lower the cost or pollution.

Under such circumstances, developing a cost effective and sustainable way to produce synthetic graphite and graphene is becoming even more attractive. For example, biomass waste is among attractive carbon sources that have been widely investigated as raw material for graphite production. The synthesis and application of biomass as carbon source have drawn attention due to it availability, sustainability and cost effective, according to Frost & Sullivan.

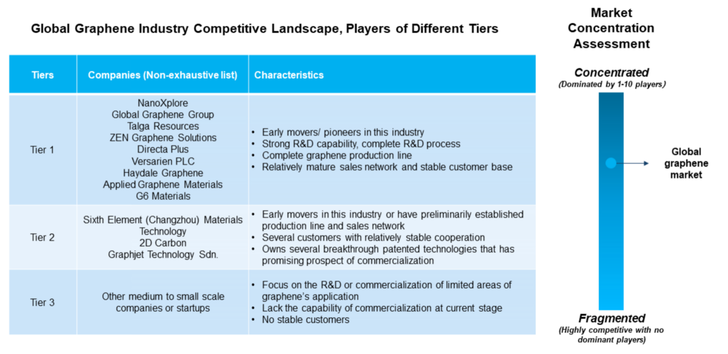

The global graphene market competition is relatively concentrated due to its high barrier to realize commercialization. Among graphene companies that have realized commercialization or substantial technology breakthrough, NanoXplore, Global Graphene Group, Talga Resources, Versarien PLC, and Graphjet are the major leading players in the industry, according to Frost & Sullivan.

Graphjet Technology Sdn Bhd was incorporated in 2019 in Kuala Lumpur, and it has the world’s first patented technology to recycle the palm kernel shells generated in the production of palm seed oil to produce single-layer graphene and artificial graphite. Malaysia is the second largest palm kernel shell waste producer, which has provided the rich raw material for Graphjet. With palm kernel-based technology, Graphjet can manufacture graphene that is of higher quality than currently available and at a price that is 80% lower than the current market price. In terms of environmental protection, the resources supply of palm kernel shell guarantee sustainable green and recyclable regeneration for the production of graphite and graphene. Due to using palm kernel shell as the raw material, the CO2 emission during the whole graphite production of Graphjet is only 2.95 kg CO2 eq which is much lower than the industry average level. At present, Graphjet has cooperated with the Massachusetts Institute of Technology (MIT) and various local universities in Malaysia, and it has become a membership of the Industrial Liaison Program (ILP). For the production capacity, Graphjet expects to open its first manufacturing plant in the Kuantan district of Pahang State with an annual output of 10,000 tons of graphite and 60 tons of graphene.

Frost & Sullivan’s White Paper for Global Graphite and Graphene Markets 2017-2026 highlights the following:

- Graphite (classification, development course, industry chain, etc.);

- Graphene (classification, technology, development course, industry chain, etc.);

- Global graphite industry (market size, etc.);

- Global graphene industry (status quo, market size, cost, patents, industrialization, development trends, etc.);

- Graphene downstream sectors (market size, segments, application, etc.);

- Introduction of Major Companies

Key Topics Covered:

- Introduction of Graphite and Graphene

- Overview of Global Development of Graphite and Graphene

- Graphite and Graphene Definition

- Graphite and Graphene development history

- Graphite and Graphene properties and characteristics

- Development status of graphene industry

- Graphite and Graphene Industry Chain Analysis

- Upstream: raw materials and supply

- Midstream: Graphite and Graphene Production

- Analysis of Graphene Preparation Technology

- Technology Advancement Analysis

- Downstream of Graphite and Graphene: Industrial Applications

- Regional Development of Graphite and Graphene

- Graphite and Graphene development in North America

- Graphite and Graphene development in Asia-Pacific

- Graphite and Graphene development in Europe

- Graphite and Graphene Global Market Size

- Graphite and Graphene global market size and forecast by applications

- Graphite and Graphene global market size and forecast by regions

- Graphene Industry Policies, Development Drivers, Trends, Restraints, Operational Risks, Entry Barriers, Investment Highlights, and Investment Advices

- Competitive Landscape

- Prominent Companies Recommended

About Frost & Sullivan

Frost & Sullivan, the Growth Partnership Company, works in collaboration with clients to leverage visionary innovation that addresses the global challenges and related growth opportunities that will make or break today’s market participants. For more than 60 years, we have been developing growth strategies for the global 1000, emerging businesses, the public sector and the investment community.

Media contact

Contact: Rachel Zhang

Company Name: Frost & Sullivan

Website: http://www.frostchina.com

Email: [email protected]

Source: Story.KISSPR.com

Release ID: 431805